LÊ TÙNG CONSTRUCTION PERSPECTIVE

The management of public investment costs and the post-auditing mechanism demand absolute transparency alongside fair legal safeguards between contractors and project management boards. According to Lê Tùng Construction, a professional cost accounting system, strict Quantity Surveying (QS) standards, and effective price risk management solutions are the universal keys to protecting project progress from macroeconomic disruptions.

When Empowered Individuals Hesitate to Decide

During the implementation of many public investment projects recently, especially amidst the strong fluctuations in construction material prices from 2021-2024 (steel prices at times surged over 30-40%, fuel and transport costs increased significantly), the application of traditional unit prices and norms has revealed a clear delay compared to market realities.

Inspecting, post-auditing quality, and settling public investment project costs.

This situation forces many investors to handle situations more flexibly: consulting market quotations; using data from similar projects; and adjusting estimates during execution.

However, precisely at these moments requiring quick decisions, the common sentiment is a reluctance to decide. The reason is not a lack of professional basis but legal risk. Amidst strict regulations for handling violations in public investment, public financial management, and bidding, the lack of a mechanism to define a “safe boundary” causes many to revert to rigid sets of norms, even knowing they are no longer suitable for current realities.

According to reports from some National Assembly discussions and public investment monitoring reports, the situation of “fear of responsibility,” “hesitation to sign,” and “waiting for guidance” still persists in many localities, directly affecting the disbursement progress of public investment funds, which for many consecutive years have not met plans (in 2023, disbursement was about 82-83% of the plan, and 2024 continues to face pressure for improvement).

A paradox has emerged: the mechanism is granting more power, but execution behavior is becoming more cautious. This shift is not accidental but clearly shaped within the legal system.

Government Decree No. 10/2021/ND-CP on the management of construction investment costs has begun to shift from a mechanism of imposing unit prices to providing reference tools such as: construction norms; construction price indices; investment capital rates.

Post-Auditing Mechanism in Public Investment Cost Management: Current Situation and Challenges

However, the real turning point lies in the Construction Law No. 135/2025/QH15, effective from July 1, 2026. This Law establishes three core principles: (i) Construction investment costs are determined based on market prices; (ii) The investor is fully responsible within the scope of the total investment; (iii) The State performs post-control through inspection and auditing based on the methods and data used.

Notably, the Law allows the use of data from similar projects, even international references, to determine costs, a fundamental change. This means the State no longer “does the work” of cost determination but shifts to framework design and supervision.

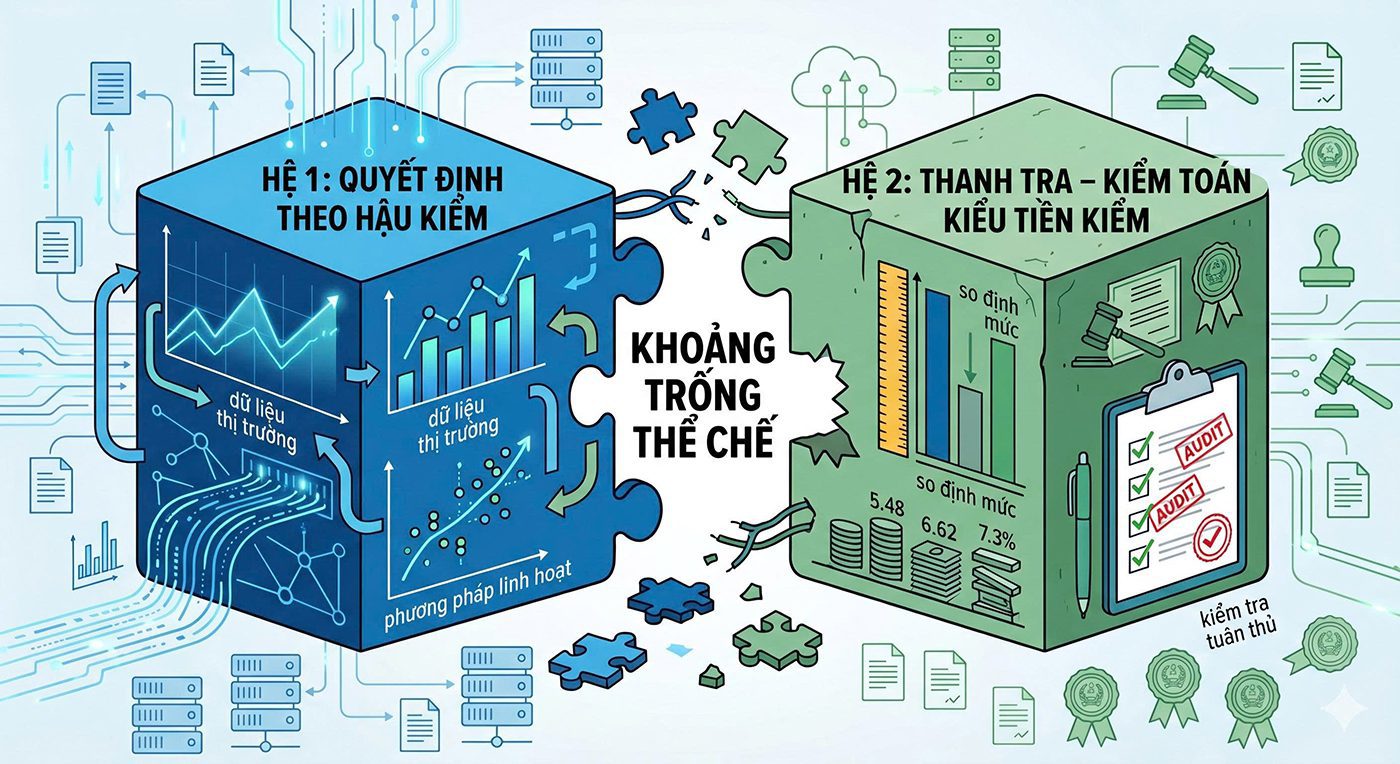

However, implementation issues arise. For many years, the system operated on the logic of: adhering to norms and procedures to ensure legal safety. When shifting to post-auditing, this logic changes: choosing an appropriate method means taking responsibility and accountability. But while powers are expanded, the mechanism for defining responsibility has not changed accordingly.

Currently, inspection and auditing activities in public investment primarily rely on: data reconciliation; comparison with norms and unit prices; and checking procedural compliance. In contrast, the post-auditing model requires evaluating: the reasonableness of the method; the quality of input data; and risk management capabilities.

This discrepancy creates an “institutional gap”: decision-making power has been decentralized, but evaluation standards still bear the imprint of pre-auditing. This is one of the key reasons leading to the avoidance mentality.

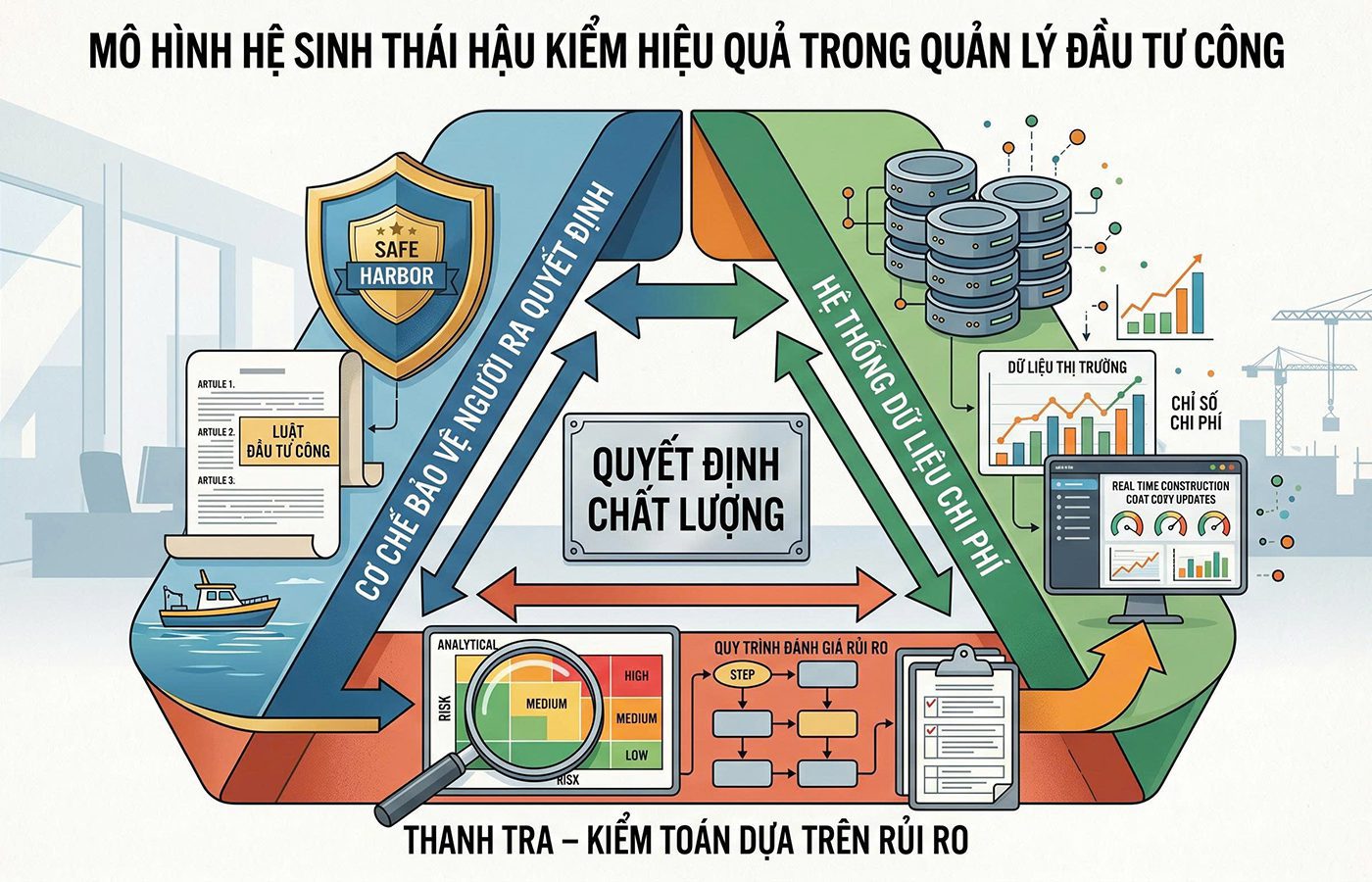

International practice shows that post-auditing cannot function without accompanying institutions.

In the United Kingdom, the cost management system is not based on rigid unit prices but uses “Should Cost Model,” a model for forecasting project whole-life costs, in the context of highly developed data systems and institutional capacity. Data is aggregated from the BCIS system with tens of thousands of projects.

The Necessity of a Legal Protection Framework for Implementing Personnel

More importantly, responsibility is individualized through the Accounting Officer mechanism. The head of the agency is accountable to Parliament for the efficiency of public spending. In case of disagreement with political decisions, they have the right to request a “Letter of Direction” to clearly establish responsibility.

Detailed process for controlling construction cost estimation norms.

In Singapore, the Public Sector Governance Act (PSGA 2018) clearly stipulates the principle of protecting public officers when performing duties with “good faith” and “due care.” This creates a “legal safe zone” for decisions under uncertainty, while still being within the framework of strict control and accountability mechanisms.

The OECD also recommends that effective public investment must be based on institutional capacity, particularly the ability to assess risks and learn from performance results.

The common point of these models is that post-auditing is only effective when there is a mechanism to protect decision-makers and a robust data system, coupled with appropriate institutional capacity and control mechanisms.

In this context, Vietnam’s problem is not whether to switch to post-auditing, but the way to transition.

Reality shows that regulations have shifted to post-auditing but the way responsibility is handled still follows pre-auditing logic. This leads to a “hybrid” state: investors are empowered to determine costs but legal risks still concentrate on the individual signatories, while evaluation criteria are unclear.

If a cost decision is based on market data but deviates from the initial estimate, is it a market risk or a violation? Does responsibility lie with the individual or the system? When these questions lack clear answers, avoidance is an understandable behavioral response.

Solutions for Balancing Authority and Responsibility in Disbursement

Based on international experience and domestic practice, three prerequisites can be identified.

First, legalizing the mechanism to protect decision-makers. Specific criteria need to be added to the Decrees guiding the Construction Law 2025 to define: what constitutes a “reasonable” decision; what is “good faith”; and the scope of immunity from responsibility when procedures have been complied with.

Second, establishing a national cost data system. Currently, data from the National E-procurement System, construction price indices from the Ministry of Construction, and localities are fragmented, lack integration, and are not effectively utilized. It is necessary to integrate them into a standard comparison system, allowing for the determination of reasonable cost margins (e.g., in some international systems, costs can fluctuate around ±10–15% compared to the industry average).

Third, innovating inspection and auditing methods. The focus needs to shift from checking the “right – wrong” of figures to evaluating the decision-making process and risk management. In volatile market conditions, deviations are inevitable; the question is whether the deviation is within the controllable range and can be explained.

Review and compensation for construction material prices for technical infrastructure workshops.

The implementation phase of Construction Law 2025 can be seen as a “testing ground.” During this period, mechanisms such as: “safe harbor”; the right to reserve opinions and request written directives; using market data as the main basis; can be piloted to gradually improve.

However, the effectiveness of these tools depends on their design being suitable for the domestic legal system and governance culture, rather than copying from international models.

More profoundly, this is not just a story of cost management, but a story of public governance. If designed correctly, post-auditing can: increase flexibility; shorten project preparation time; and enhance capital utilization efficiency.

Conversely, if accompanying institutions are lacking, it can lead to: a fear of responsibility; delayed decisions; reduced investment efficiency. Therefore, the problem is to build a system in which decision-makers have a sufficient basis to act and sufficient protection to be held accountable.

Transitioning to post-auditing is an inevitable trend in Vietnam’s public investment management reform. However, if the mechanism for protecting responsibility and the data system are not simultaneously perfected, the empowerment will struggle to be substantive. In this context, the biggest challenge is not amending regulations, but building institutional trust, so that those who are empowered truly dare to decide.

Original article source: Construction Magazine